About 2 years ago, I wrote a post on my Preference for Regular Payout Insurance. The reasons for this preference are discussed in that post, but I will further illustrate the reasons below again. At that time, I thought that such insurance policies only exist for disability income. For more traditional insurance policies covering death and critical illness, there was none. Recently it turns out that some insurer has heed the call and came up with an insurance policy covering death, terminal illness, total and permanent disability, and critical illness that pays out a regular sum each month. The insurance policy is MyFamilyCover (MFC) from Aviva. Thanks to comments from a reader, E H, on My Considerations on Eldershield, I chanced upon it on compareFIRST.sg, the official website set up by Consumers Association of Singapore, Monetary Authority of Singapore, Life Insurance Association Singapore and MoneySENSE to assist consumers to compare and find life insurance products most suited to their needs.

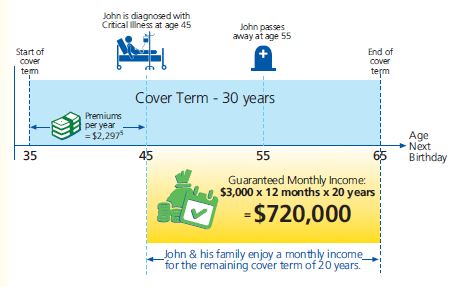

How MFC works is that you choose how much is the monthly benefit payout and the policy duration. Upon the occurrence of an unfortunate event, the policy will pay the monthly benefit for the remaining duration of the policy or 10 years, whichever is longer. An illustration of how it works is shown below.

|

| How MyFamilyCover Works |

In the example above, John enters into a policy that pays $3,000 per month for a duration of 30 years at age 35. At age 45, he is diagnosed with a critical illness. The policy will pay out $3,000 per month for the remaining duration of 20 years to him or his family. This helps the family to meet the daily expenses until say, the children have grown up and are able to earn an income to support the family.

There are 4 different flavours of the policy, as follows:

- Plan 1 - Covers Death, Terminal Illness (TI), Total & Permanent Disability (TPD) and Critical Illness (CI)

- Plan 2 - Covers Death, TI and TPD

- Plan 3 - Covers Death and TI

- Plan 4 - Covers TPD and CI

The policy that I bought is Plan 4. However, for ease of comparison with other traditional insurance policies, I will assume Plan 1 in the subsequent discussion.

As the total amount of payout reduces with time, it is quite similar to a reducing term insurance whose sum assured reduces with time, like the loan principal of a mortage loan. How does MFC compare with a reducing term insurance? The following assumptions are used:

| MyFamilyCover | |

| Monthly Cover | $ 3,000 |

| No. of Years | 30 |

| Reducing Term Insurance | |

| Total Cover | $ 1,000,000 |

| No. of Years | 30 |

| Interest Rate | 5.0% |

The reduction in total payout for both MFC and Reducing Term is shown below.

|

| Total Payout for MFC and Reducing Term Insurance Over Time |

As shown in the figure above, the total payout for MFC drops faster than Reducing Term as Reducing Term has an interest rate of 5%. The difference reaches $145,000 by Year 18, after which the difference reduces over time. As MFC has a minimum payout duration of 10 years, the total payout remains constant at $360,000 from Year 20 onwards while that for Reducing Term continues to drop. From Year 24 onwards, the sum assured for MFC is higher than that for Reducing Term.

Why did I choose MFC over a more traditional Reducing Term insurance, even though Reducing Term has a higher payout than MFC for most of the policy duration? The key reason is because MFC pays out the benefits regularly whereas Reducing Term pays out the benefits in a lump sum, even though the lump sum may be higher. While the lump sum payout guarantees the amount of payout received, it does not guarantee how much money could be spent monthly to meet daily expenses or how long the money could last. In contrast, for MFC, both the amount that could be spent monthly and how long the money could last are known. Considering a typical family in which the spouse might not be financially savvy, the parents are old and the children are young, a known regular payout for a known duration provides much greater assurance to the family than a known lump sum payout but unknown draw-down amount and unknown duration. Not everyone is financially savvy to be able to manage a lump sum payout. If the family unwittingly invests the lump sum payout into some risky investments in their attempt to stretch the duration which the money could last, it could put the financial sustainability of the family at risk. For the above reason, I have always preferred a regular payout insurance over a lump sum payout insurance. It is good that Aviva has understood the need and came up with an innovative insurance policy that addresses the needs more precisely. I hope more insurers would do the same.

There is currently a 20% discount on all future premiums on MFC. The promotion will end on 31 Jul. So, if you are interested, do hurry. You can contact Aviva on their website (give 2 days for them to call you back). Alternatively, I can refer you to the insurance agent whom I bought MFC from by leaving your contact info here. In the meanwhile, you can check the MFC brochure on Aviva website and the annual premiums on compareFIRST.sg.

By the way, when you meet the insurance agent, please let them know that you found out about MFC on compareFIRST, so that insurers can place more of their insurance products on it for comparison.

See related blog posts:

No comments:

Post a Comment