The massive sell-down in Mar brought many REITs to rare, multi-year lows. This re-ignited my interest in REITs, as I have been out of them for many years due to their increasing debt levels and decreasing yields. However, I passed up the opportunity while I analysed what could be the impact of COVID-19 on REITs. Despite the massive government interventions, things do not look good for retail and F&B companies. And when tenants struggle, their landlords will also suffer. In this blog post, I will examine the potential impact of COVID-19 on 2 retail companies and 2 F&B companies.

Before we begin, it is good to recap what are the measures the government has taken to cushion the impact on retail and F&B companies.

Wage Support

Through 4 extraordinary budgets, the government will provide support to wages via the Job Support Scheme (JSS). The level of wage support varies across industries. The JSS will last for 10 months. For the first 2 months, it will cover 75% of $4,600 of wages of all local employees for all companies. The 75% support level will continue if companies are not allowed to operate during the gradual lifting of Circuit Breaker, until Aug. For the remaining months, the wage support will be as shown in Fig. 1 below.

|

| Fig. 1: JSS Support for Remaining Months |

Thus, both retail and F&B companies will get the following wage support:

- 3 months of 75% wage support (assuming they are allowed to reopen in Jul)

- 7 months of 50% wage support

This

translates to 48% reduction in annual wage costs for FY2020 (assuming that all wages of employees are at $4,600).

Rental Relief

In addition to wage support, the government has also implemented measures to help companies cope with rental costs. The Government will provide property tax rebates and cash grants equivalent to 2 months' rent for qualifying commercial properties and 1 month's rent for industrial and office properties for Small and Medium Enterprises (SMEs) with annual turnover of less than $100M. On top of that, the government also passed a law requiring landlords to waive 2 months' rent for commercial properties and 1 month's rents for industrial and office properties for SMEs that have seen a significant drop in their monthly revenues. The total amount of rental relief for SMEs in commercial and industrial/ office properties is summarised in Fig. 2 below.

|

| Fig. 2: Rent Relief for SMEs |

Thus, retail and F&B SME companies will get up to 4 months of rental relief, translating to a 33% reduction in annual rental costs for FY2020.

Revenue Hit

COVID-19 has stopped people from shopping and dining out, either because of government-mandated lockdowns or fear of contracting the virus. It is anyone's guess how soon people will go back to their normal lifestyles after shops and F&B outlets are allowed to operate. China is the first country to exit the lockdown and provides the first glimpse of how consumers would react in a post-COVID world. Figs. 3 and 4 below from Capitaland Retail China Trust's (CRCT) investor conference in May shows that shopper traffic is only picking up gradually after the end of the lockdown. Year-on-year, total shopper traffic and tenants' sales in 1Q2020 declined by 37.6% and 42.5% respectively.

|

| Fig. 3: Shopper Traffic at CRCT Malls in 1Q2020 |

|

| Fig. 4: Tenants' Sales at CRCT Malls in 1Q2020 |

For the revenue hit on retail and F&B companies, I assume the following:

- 3 months of closure during Circuit Breaker: 0% revenue

- 2 months of gradual re-opening: 50% revenue

- 7 months of recovery: 80% revenue

This translates to a 45% decline in annual revenue for FY2020. Will retail and F&B companies survive this kind of harsh business conditions? Let us take a look at 2 retail companies and 2 F&B companies.

Retail Companies

Company F

Company F is a barely profitable retail company. In FY2019, it generated net profit of $0.2M. See Fig. 5 below for its income statement for FY2019.

|

| Fig. 5: Company F's Income Statement for FY2019 |

It is insightful to note that of the gross profit of $64.7M, staff costs ($21.4M) take up 33% of the gross profit and rental costs ($22.3M) take up another 34% of the gross profit. In total, staff and rental costs take up 68% of gross profit. It is no wonder that the government had to act quickly to relieve the pressure of staff and rental costs on companies!

Applying the estimated declines in revenue, staff and rental costs above (plus some other assumptions for other costs), Company F might see its net profit turn from positive $0.2M to negative $5.4M. See Fig. 6 below for the computation.

|

| Fig. 6: Estimated Impact of COVID-19 on Company F |

As at end FY2019, Company F had cash of $7.8M. The estimated loss of $5.4M is equivalent to 69% of its cash and 10% of its equity.

Company C

Company C is a fairly profitable retail company. In FY2019, it generated net profit of $17.7M. Applying the same analysis as Company F, Company C might see its

net profit reduced from $17.7M to $9.1M. See Fig. 7 below

for the computation. Company C will likely have no problem going through the COVID-19 situation.

|

| Fig. 7: Estimated Impact of COVID-19 on Company C |

F&B Companies

Company S

Company S is a barely profitable F&B company. In FY2019, it generated net profit of $0.8M. See

Fig. 8 below for its income statement for FY2019.

|

| Fig. 8: Company S's Income Statement for FY2019 |

Like retail companies, staff and rental costs take up a large portion of the gross profit of F&B companies. Staff costs ($14.3M) take up 43% of gross profit and rental costs ($7.9M) take up another 24% of gross

profit. In total, staff and rental costs take up 66% of gross profit.

Applying the same analysis, Company S might see its

net profit turn from positive $0.8M to negative $2.6M. See Fig. 9 below

for the computation. The estimated loss is equivalent to 32% of its cash and 27% of its equity as at end FY2019.

|

| Fig. 9: Estimated Impact of COVID-19 on Company S |

Company J

Company J is a fairly profitable retail company. In FY2019, it generated

net profit of $10.9M. Applying the same analysis as Company F, Company J

might see its

net profit reduced from $10.9M to $1.9M. See Fig. 10 below

for the computation. Company J will likely have no problem going through

the COVID-19 situation.

|

| Fig. 10: Estimated Impact of COVID-19 on Company J |

Conclusion

We have run through the estimated impact of COVID-19 on 2 retail and 2 F&B companies. Staff and rental costs consistently take up around 2/3 of gross profits. When there is no or poor business due to government-mandated lockdowns or fear of contracting the virus, the impact on the bottom lines of retail and F&B companies is very significant. As in all crises, stronger companies with leaner cost structures and/or significant retained earnings will be able to weather the storm while weaker ones will end up in losses, despite the extraordinary government interventions.

The companies I analysed above are all listed companies. How about unlisted companies? Would they have stronger financials than listed companies? Some food for thoughts.

Last week, Department of Statistics released the retail and F&B sales figures for Apr 2020. Fig. 11 below shows that retail sales declined by 13.3% in Mar (before Circuit Breaker) and 40.5% in Apr (during Circuit Breaker) on a year-on-year basis. Almost all sectors were impacted, with the exception of Supermarts & Hypermarts, Mini-marts & Convenience Stores, and to some extent, Computer & Telco Equipment.

|

| Fig. 11: % Changes in Retail Sales |

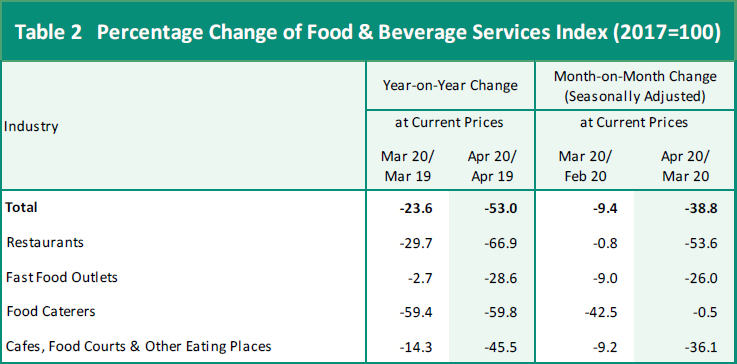

Fig. 12 below paints a similarly bleak picture for F&B sales, with a decline of 23.6% in Mar and 53.0% in Apr on a year-on-year basis. No F&B sector escaped the decline.

|

| Fig. 12: % Changes in F&B Sales |

Lastly, Fig. 13 below shows the tenant mix at Frasers Centrepoint Trust's Malls.

|

| Fig. 13: Tenant Mix at Frasers Centrepoint Trust's Malls |

F&B accounts for 38% of Gross Rental Income. Fashion takes up 14% while Beauty & Health accounts for 11%. All these sectors will be impacted by COVID-19. The only sector that has a roaring business during COVID-19, Supermarts & Hypermarts, contributes only 5% of the Gross Rental Income.

In conclusion, COVID-19 has resulted in a very challenging business environment for retail and F&B companies. When tenants struggle, landlords will also suffer. Things do not look good for retail landlords.

P.S. I am vested in Capitaland.

See related blog posts: