Last year, First Reit's share price had been dropping since the COVID-19 outbreak and the announcement by its sponsor, Lippo Karawaci (LPKR), to

restructure the master leases of the hospitals that it lease from First

Reit. The low share price attracted my attention, but when First Reit

announced that the rents would be paid in Indonesian Rupiah (IDR) instead of

Singapore Dollars (SGD) in future, I was no longer interested. Having the

rents paid in IDR instead of SGD would subject it to foreign exchange risks.

Not only that, the assets would be devalued in line with the depreciation of

IDR while the liabilities would continue to be in SGD. This would lead to a

sharp drop in Net Asset Value (NAV). This was exactly what happened to

another REIT with Indonesian assets, Lippo Malls Indonesia Retail Trust,

when IDR depreciated sharply against SGD in 2013. First Reit, however, was

not affected then as its rent revenue was pegged to SGD instead of IDR. See

A Tale of 2 Indonesian REITs

for more details.

Arising from the lease restructuring, First Reit's revenue in FY2019 will

drop from SGD115.3 mil to SGD77.6 mil. 73% of this revenue (SGD56.7 mil)

will be paid in IDR. NAV will also drop from $1.00 to $0.52. Leverage will

correspondingly rise from 34.5% to 47.9%. In addition, lenders are

uncomfortable with the sustainability of First Reit's capital structure and

decided to only refinance SGD260 mil out of the SGD400 mil loan, of which

the first tranche of SGD196.6 mil will mature on 1 Mar 2021. First Reit has

proposed a 98-for-100 rights issue at a heavily discounted price of $0.20 to

bridge the funding gap of SGD140 mil. Post rights issue, NAV will drop to

$0.36 while leverage will drop to 33.9%.

While I do not own First Reit, my family has it. Thus, a key question we

have been discussing is whether to subscribe for the rights and give First

Reit another chance. Will it be throwing good money after bad, or will it be

a rare opportunity to invest more money in a REIT that had provided good,

regular distributions for the past 13 years?

As part of the lease restructuring, the Base Rent for hospitals leased to

LPKR and Metropolis Propertindo Utama (MPU), a related company to LPKR, will

be reset from SGD92.2 mil in FY2019 to IDR613.1 bil (equivalent to SGD56.7

mil at an exchange rate of SGD1:IDR10,830) in FY2021. The Base Rent will

increase annually at a rate of 4.5%. In addition, there will be

a Performance Based Rent pegged at 8% of the hospitals' Gross Operating

Revenue. The rent payable will be the higher of the Base Rent and the

Performance Based Rent, on an asset-by-asset basis.

Opportunities

Although the rents for the Indonesian hospitals will be paid in IDR instead

of SGD in future, the Performance Based Rents are likely to provide some

upside. Fig. 1 below shows that the revenue of Siloam International

Hospitals, which leases the hospitals from LPKR, MPU and First Reit as the

end user, has been increasing since 2011.

|

|

Fig. 1: Revenue of Siloam Hospitals International |

Siloam also reports the revenue of its major hospitals in its annual reports. Fig. 2 below shows the total revenue and rent paid by LPKR to First Reit for hospitals which revenue data is available from FY2014 to FY2019.

|

| Fig. 2: Revenue and Rent Paid to First Reit for 6 Hospitals |

The figure shows that the revenue in IDR has increased at an annual rate of 12.2% from FY2014 to FY2019. When converted to SGD, the revenue has increased at an annual rate of 10.4%. Over the same period, IDR has depreciated against SGD by an average of 1.6% annually. In contrast, the rent paid to First Reit has stayed constant.

Assuming revenue in IDR in FY2021 recovers to the same level as FY2019 after COVID-19 and continues to grow at an annual rate of 10% from FY2021 to FY2035, the Base Rent and Performance Based Rent in IDR will be as shown in Fig. 3 below.

|

| Fig. 3: Projected Base & Performance Rent in IDR |

From Dec 2006 when First Reit was first listed till now, IDR has depreciated

against SGD at an average rate of 4.3%. Assuming this historical depreciation

rate continues, when converted to SGD, the Base Rent and Performance Based

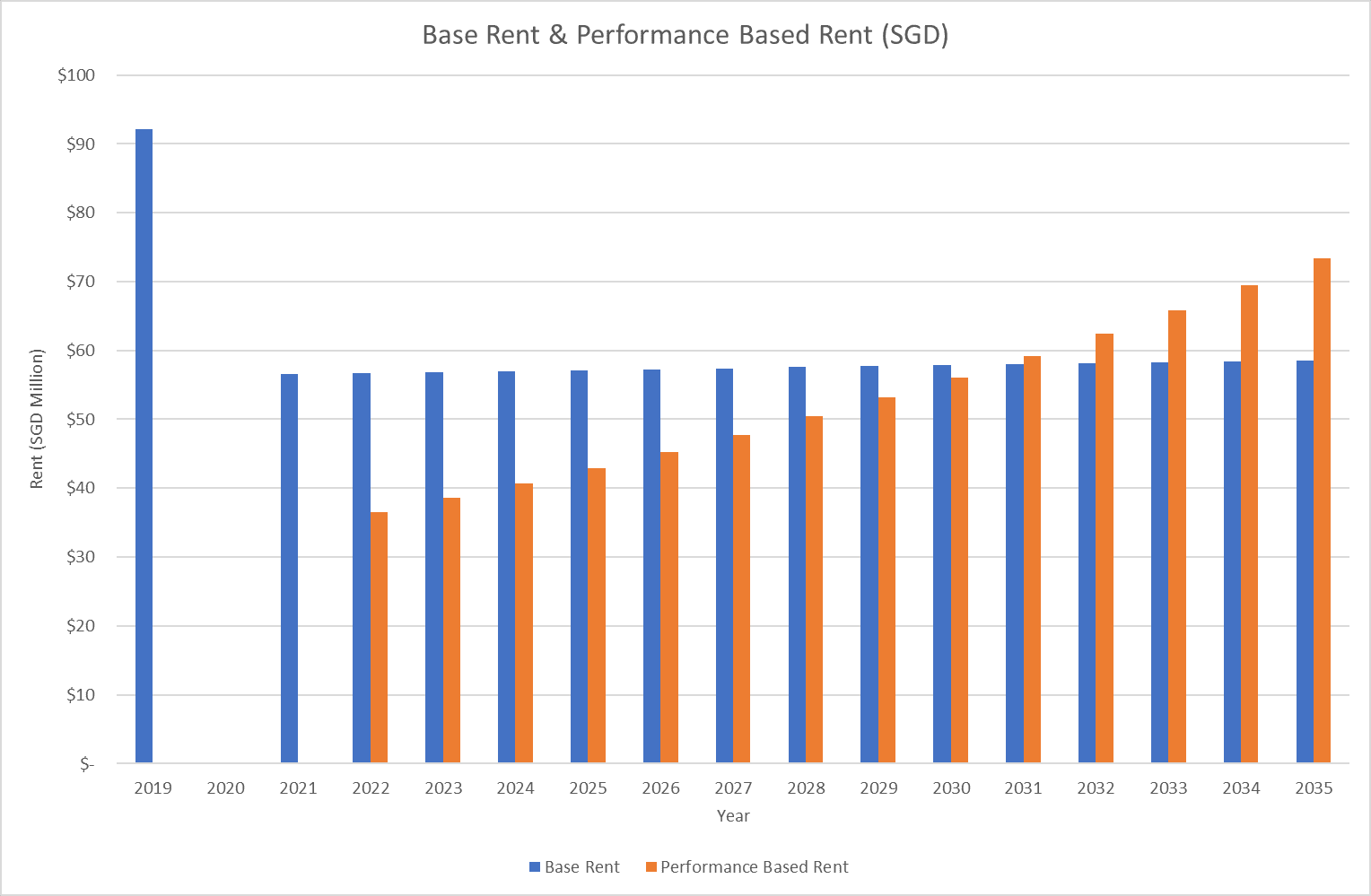

Rent in SGD will be as shown in Fig. 4 below.

|

| Fig. 4: Projected Base & Performance Rent in SGD |

Based on Fig. 4, the projected Base Rent in SGD will largely stay flat as the annual rent increase of 4.5% barely outstrips the historical IDR depreciation rate of 4.3%. Performance Based Rent in SGD is projected to exceed the Base Rent in 2031. It is projected to reach SGD73.3 mil in FY2035 when the leases expire, 20% short of the existing Base Rent of SGD92.2 mil in FY2019. If this revenue growth materialises, it will provide some upside to the Distribution Per Unit (DPU) in the last 5 years of the 15-year leases.

Without the revenue growth, DPU will be around 2.59 cents immediately after the lease restructuring and rights issue. Maintaining the DPU at this level requires other risks not materialising in future.

Risks

There are plenty of risks with this investment. The first and foremost is whether LPKR and MPU will continue to face financial difficulties and default on the rents payable to First Reit. If that is the case, all bets are off. Its Indonesian assets which are leased to LPKR, MPU and Siloam, including those not subject to the current lease restructuring, comprise 95% of its assets post-restructuring. These assets will be significantly impaired. First Reit will likely default on its loans.

The second risk is the currency mismatch between its assets of which 81% are

valued in IDR and loan liabilities which are in SGD. This is the same problem

encountered by Lippo Malls when IDR depreciated sharply against SGD in 2013.

It is important to monitor whether First Reit will take steps to minimise the

currency mismatch by converting the SGD loans to IDR loans. Entering into

forward contracts to hedge the IDR receivables into SGD is another option, but

there is a limit to the no. of years you can hedge. Hopefully, there is no

sharp depreciation around the time loans mature and First Reit enters into

discussions with banks for refinancing.

The third risk is that after the current SGD400 mil loan has been refinanced with the rights issue, there remains another SGD100 mil loan due in May 2022. The concern is whether First Reit is able to refinance this loan in full. If it is unable to, there is risk of another rights issue.

However, I am not too concerned with this loan. The existing SGD400 mil loan was a syndicated loan from OCBC while the SGD100 mil loan was from OCBC and CIMB jointly. The new SGD260 mil loan to partially refinance the SGD400 mil loan is also from OCBC and CIMB jointly. That means that the 2 banks have considered First Reit's ability to repay the SGD100 mil loan when they decided to offer the new SGD260 mil loan to First Reit. My guess is when it is time to refinance the SGD100 mil loan, both OCBC and CIMB will come together again.

Having said the above, the ability to refinance the SGD100 mil loan depends greatly on whether there are any other adverse developments affecting First Reit's ability to collect rent from its assets, such as whether LPKR's and MPU's financials continue to deteriorate further, or whether there is a sharp depreciation in IDR that is unhedged.

The fourth risk is there is a SGD60 mil perpetual securities that is due to reset its distribution rate on 8 Jul 2021. Usually, companies will choose to redeem the perpetual securities and issue new ones to replace them. However, given First Reit's financial conditions, it will likely not redeem the perpetual securities when the distribution reset date comes. Non-redemption does not constitute default. Furthermore, given the low interest rate environment, the distribution rate will likely be lower after reset. The current distribution rate is 5.68%. The distribution rate will reset to 5-year SGD Swap Offer Rate (SOR) + 3.925%.

Distribution on the perpetual securities is also discretionary. Non-payment

of distribution does not constitute a default. However, distributions on the

Reit units will need to be stopped. The annual distribution on the perpetual

securities is SGD3.41 mil.

The fifth risk is besides the 14 Indonesian hospitals that are subject to lease restructuring, there are other assets whose leases are due to expire. The lease on Sarang Hospital will expire on 4 Aug 2021. The current annual rental is USD0.7 mil. Although there is an option to renew for another 10 years, likely it will be renewed at a lower rental rate. The hospital was purchased for USD13.0 mil in 2011. The latest appraised value is only USD4.6 mil in 2020, which suggests lower rental rate going forward. First Reit has also flagged that there will be upcoming capital expenditure, and further marked down the value to USD3.1 mil.

As mentioned in last week's blog post on

What Siloam's Financial Reports Can Tell Us About First Reit's Lease

Restructuring, there is another Indonesian hospital which is leased directly to Siloam

which could be subject to lease restructuring or lower rental when the lease

expires in Dec 2025. The annual rent for this hospital is SGD4.2 mil.

The sixth risk is that after the lease restructuring, the leases of the 14

Indonesian hospitals will be extended to Dec 2035. Fig. 5 below shows the

new lease expiry profile.

|

|

Fig. 5: Revised Lease Expiry Profile |

An unintended consequence of this lease extension is that there is now a concentration of lease expiry. 66% of all leases by GFA will now expire in Dec 2035 instead of being fairly distributed. If First Reit is not able to buy new properties to diversify the geographical, tenant and lease expiry concentrations, there will be another round of concern when Dec 2035 comes near.

Conclusion

The lease restructuring is a painful exercise for existing shareholders. However, there are silver linings in the form of higher rents through Performance Based Rent towards the end of the 15-year leases. Nevertheless, even if the restructuring and rights issue go through smoothly, there are still road bumps and risks down the road for First Reit.

Should First Reit be given a second chance? I cannot advise you what you should do, but for us, we are inclined to give it a small second chance. We will monitor how First Reit manages the risks identified above, and if it does well, increase the chance given to it.

See related blog posts:

Hi Chin Wai

ReplyDeleteIs this a deep value play whereby you determine the valuation is so attractive to the point that the margin of safety compensates for the cash flow problems?

Considering REITs is just a structure to extract rental parents from tenants, wouldn't it be easier to look for higher quality REITs and handle the capital appreciation portion in your spicy ETF portfolio?

Hi INTJ,

DeleteI would consider it as a distressed play. The size will be small so that if the investment does not turn out well, the loss is controlled. On the other hand, if it turns out well, returns will be handsome.

Hi 2.59 DPU post restructuring is highly unlikely to materialise. This is because the new lease depends on either the base rent or 8% of revenue. In fact in First REIT presentation, they mention the 1H2020 performance under the new tenancy yields only 0.55 cents DPU.

ReplyDeleteI do think this will improve in 2021 onwards but unlikely to be 2.59 cents and will not be 1.1 cents (the worst case scenario). Personally, my estimation bis that it will be 1.6 cents DPU and basing my own valuation this DPU for 8% yield

Hi Choon Yuan,

DeleteThe DPU of 2.59 cents is a proforma figure extracted from the rights issue announcement. Nevertheless, I agree with you that the actual DPU will likely be lower as there are many risks along the way.

I have lost trust in the manager's ability to run this REIT, and lost trust in the main tenant, Karawaci, to reliably pay the rent.

ReplyDeleteOnce bitten, twice shy.

Hi Boring Investor,

ReplyDeleteThis is surely a more exciting stock that you have nibbled on. Are you planning to subscribe to the rights issue ? I feel there is not much additional discount at the risk of doubling the exposure to the stock.

In addition there are news reports that

1) Faster turnovers and higher capacity rates at private hospitals during the peak of COVID. (which Indonesia is now at)

2) Lower chances of default for LPKR (https://www.fitchratings.com/research/corporate-finance/fitch-revises-outlook-on-lippo-karawaci-to-stable-affirms-b-upgrades-national-rating-28-01-2021)

What are your views on this ?