Properties are the favourite investment class in land-scarce Singapore. Many people have heard and seen for themselves how a flat that cost their parents a few thousand dollars in 1960s could rise to hundreds of thousand dollars currently. The conventional wisdom is that land is scarce in Singapore, therefore, property prices has only one way to go, which is up.

I'm not a property investor. However, I did researched about the prospects of property investment in the long-term 10 years ago, and my conclusion was that it was not ideal to hold on to properties past the year 2017. This point was shared in a letter to the Straits Times Forum Page in response to a Special Report titled “Can

You Afford to Retire?” on 18 Dec 2004. Because of this research, I have avoided property investment and missed the great property boom experienced in the last couple of years. I'll share the findings here for discussion.

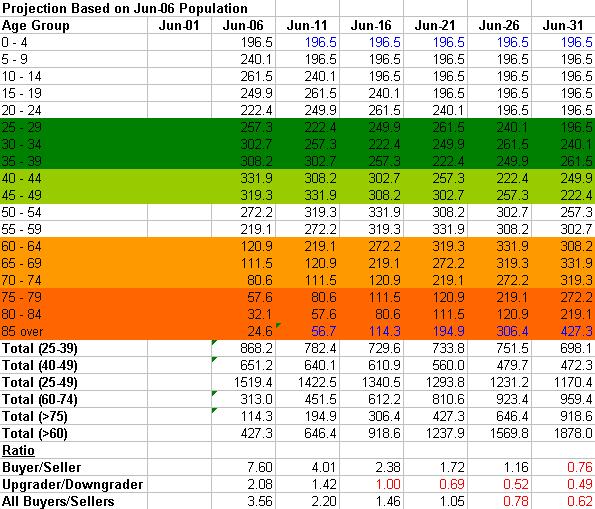

The primary reason for property investment not being an ideal investment in the long-term has to do with the population demographics of Singapore, which by now, everyone knows is ageing rapidly. Below are the population projections in Jun 2001, at the time of my research. The population projections in the subsequent years are obtained by shifting the 2001 population forward, i.e. the population aged 0 - 4 in 2001 would be aged 5 - 9 in 2006, 10 - 14 in 2011, so on and so forth. The birth rates in subsequent years are maintained at the prevailing levels.

|

| Figure 1: Population Projections Based on 2001 Population Statistics |

Let's assume that the house-buying population is aged 25 - 39, the upgrader population is aged 40 - 49, the downgrader population is aged 60 - 74 and the house-selling popuation is aged 75 and above. To simplify the analysis, let's further assume that there is no net migration and no new houses built. The ratio of potential buyers/ upgraders to potential sellers/ downgraders is a healthy 4.02 in 2001, which means that there are 4 potential buyers/ upgraders for every potential seller/ downgrader. This is a good time for holding property investments. However, this ratio decreases rapidly with time and crosses parity in the year 2020, making property investments less attractive in the long-term.

How would the ratios change if we consider net migration and new houses being built? The ratios would be more favourable with migration as there would be more buyers. On the other hand, the ratios would be less favourable with new houses built as there would be more sellers. It is unclear which of these factors would play a bigger role. Given the uncertainty of the impact of these factors and that they partially offset each other, we can leave them out of the analysis for now.

With the advantage of hindsight, we can review the same analysis using the population statistics in 2006 and 2011. The results are shown below.

|

| Figure 2: Population Projections Based on 2006 Population Statistics |

|

| Figure 3: Population Projections Based on 2011 Population Statistics |

As you can see, the ratios have improved, due to increased migration over the years. For all buyers/sellers, the year that the ratio will cross parity has increased from 2020 (based on 2001 population statistics) to 2022 (2006 statistics) to 2025 (2011 statistics). Nevertheless, the fact that sellers will eventually outnumber buyers remains unchanged. Property investors are facing a significant headwind from demographics in the long run.

To improve the situation, the demographics challenge needs to be improved, with more babies and/or migration. In addition, there should be a means to buy back houses from the elderly population who wishes to monetise their flats to fund their retirement. The lease buy-back scheme in which HDB buys back the tail-end of the lease is a good solution. Allowing residential real estate investment trusts (REITs) to be set up to buy-and-leaseback the flats to elderly (with safeguards) might be a feasible option too.

It is interesting to note that the old Chinese saying, "to raise children to guard against old age", is still as apt as ever in today's challenging demographics environment.

See related blog posts:

See related blog posts:

No comments:

Post a Comment