On 28 Dec 2020, First Reit dropped a bombshell by announcing a major rights issue at a heavily discounted price. This caused the share price to dropped significantly. The main reason is the proposed restructuring of master leases that First Reit have with Lippo Karawaci (LPKR) and Metropolis Propertindo Utama (MPU). First Reit leases hospitals to LPKR and MPU which in turn lease them to Siloam International Hospitals. The proposed lease restructuring would reduce the Base Rent of LPKR-leased hospitals from SGD80.9 mil to SGD50.9 mil and that of MPU-leased hospitals from SGD11.3 mil to SGD5.8 mil. These represent a reduction of 37% and 49% respectively. Not only that, the rents will be paid in Indonesian Rupiah (IDR) instead of Singapore Dollar (SGD) in future. As a result of the reduced revenue, First Reit's lenders have decided to only refinance SGD260 mil out of the SGD400 mil term loan, of which the first tranche of SGD196.6 mil will mature on 1 Mar 2021.

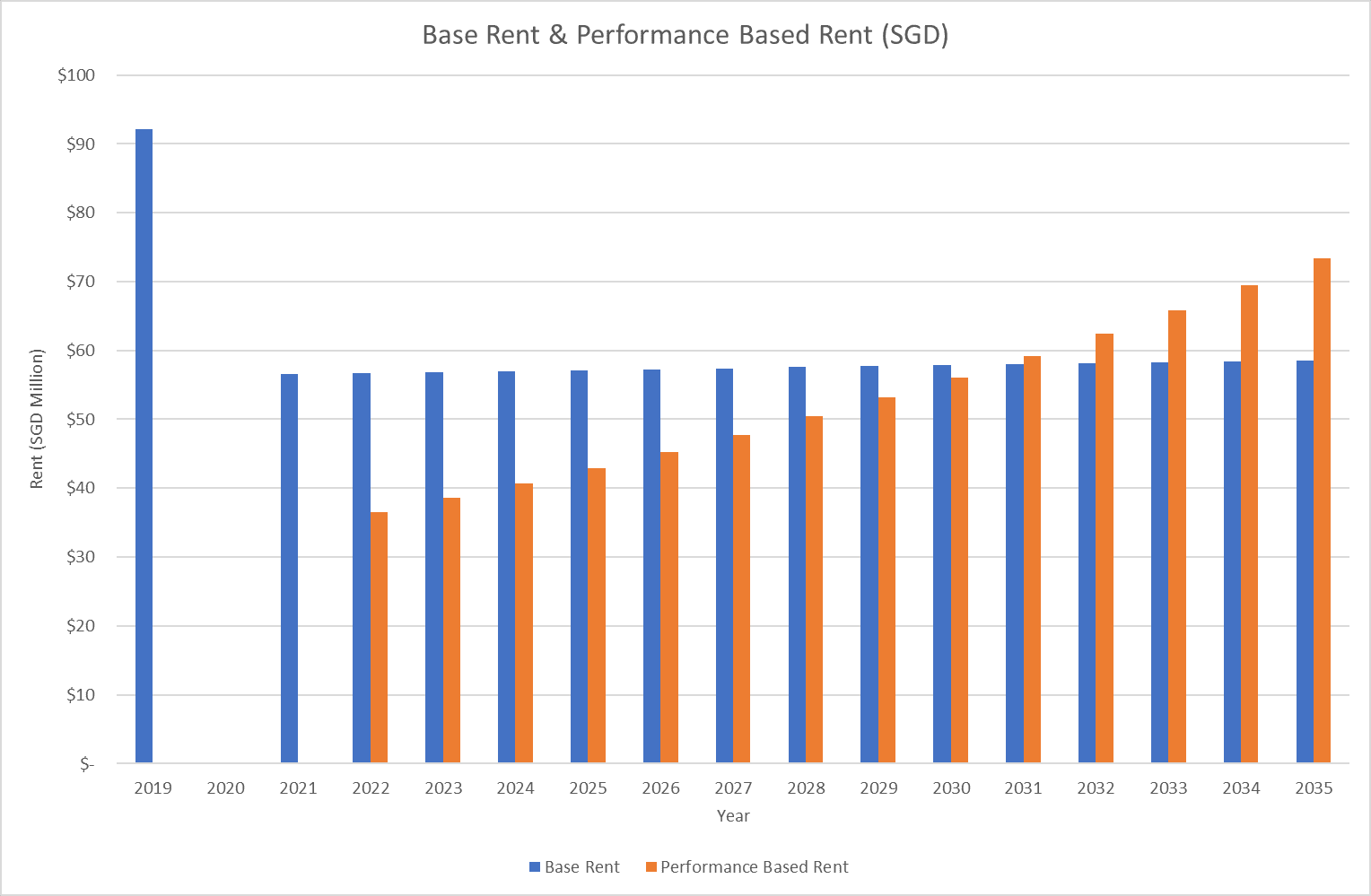

To sweeten the deal, the restructured master leases would include a fixed rental escalation of 4.5% per year, instead of 2 times Singapore's Consumer Price Index (CPI), but capped at 2% per year. In addition, there will a Performance Based Rent pegged at 8% of the hospitals' Gross Operating Revenue. The actual rent will be the higher of the Base Rent and Performance Based Rent.

Siloam is listed on the Indonesia Stock Exchange, hence its financial reports are publicly available. As the Indonesian hospitals are all leased to Siloam as the end user, and we can cross check the information from Siloam's financial reports to understand better the proposed lease restructuring.

Siloam's Annual Report for Financial Year 2019 documents the rent that Siloam pays to LPKR and MPU for the hospital leases. See Fig. 1 below. For the 14 hospitals that are subject to lease restructuring, Siloam paid a total of IDR156.8 mil to LPKR and MPU in FY2019. In contrast, the total existing and proposed commencement Base Rent paid by LPKR and MPU to First Reit is IDR997.6 mil and IDR613.1 mil respectively. The rent paid by Siloam is only 15.7% of the existing Base Rent and 25.6% of the proposed commencement Base Rent. This shows that post-restructuring, LPKR and MPU are still subsidising Siloam's rent and/or topping up First Reit's revenue. Since the hospital leases are not revenue neutral to LPKR and MPU even after lease restructuring, there is a risk that LPKR and MPU could seek another lease restructuring in future.

|

| Fig. 1: Siloam's Rent to LPKR and MPU as % of Existing & Restructured Base Rents |

Siloam's annual report also documents the Gross Operating Revenue (GOR) generated at some of its major hospitals. See Fig. 2 below. Pre-restructuring, the GOR as a percentage of existing Base Rent ranges from 7.5% to 40.7%. Post-restructuring, the GOR as a percentage of proposed commencement Base Rent ranges from 6.7% to 14.8%. For hospitals which data is available, the weighted GOR is 18.7% of existing Base Rent and 11.6% of the proposed commencement Base Rent.

This information also tallies with the information provided by First Reit during the investor dialogue on 7 Jan 2021. To a shareholder question, First Reit replied that the proposed Base Rent in aggregate is in the range of 10% to 15% of the GOR for LPKR-leased hospitals in FY2019.

|

| Fig. 2: Existing & Restructured Base Rents as % of Hospital Revenue |

Under the proposed lease restructuring, the actual rent will be the higher of the Base Rent or Performance Based Rent, which is pegged to 8% of the GOR, on an asset by asset basis. Based on the financial performance of the hospitals in FY2019, a slightly higher rent could be expected from a few hospitals, namely Kebon Jeruk, Surabaya, Purwakarta and Sriwijaya. However, take note that this is based on the financial results in FY2019, which does not include the impact of COVID-19. COVID-19 has affected the hospital revenue significantly as patients defer their visits to hospitals to avoid exposure to COVID-19.

Amid the uproar regarding the proposed lease restructuring for 14 Indonesian hospitals, one other Indonesian hospital is actually not subject to lease restructuring. The hospital is Lippo Cikarang. This hospital is leased directly from First Reit to Siloam. Siloam's annual report also shows that it is paying much higher rent on this hospital compared to those on the other 14 hospitals, i.e. there is no rent subsidy and/or top-up by LPKR and MPU.

A check on the history of the lease of this hospital shows that the hospital was acquired by First Reit in Dec 2010. At the time of purchase, the hospital was purchased from and leased back to a subsidiary of LPKR. Some time from then till now, Siloam acquired the subsidiary. Hence, Siloam is paying rent on Lippo Cikarang directly to First Reit, unlike the other 14 hospitals.

The key question to the lease restructuring is what are the true market rents for the Indonesian hospitals? Is it close to the rent paid on Lippo Cikarang which is comparable to the existing Base Rent of the other 14 hospitals, or close to the proposed commencement Base Rent of the 14 hospitals? If it is the former, the proposed lease restructuring is disadvantaged to First Reit as it will now receive below-market rent. If it is the latter, LPKR and MPU have been topping up the rent for First Reit's benefit and the restructuring might be more equitable to all parties, although painful for First Reit. It also suggests that Lippo Cikarang might have to undergo a lease restructuring at some time in future.

Siloam's annual report also shows the net profit at its major hospitals. See Figs. 3 and 4 below. Take note that the net profits are based on the rents Siloam paid to LPKR and MPU and not the top-up rents paid by LPKR and MPU to First Reit.

|

| Fig. 3: Revenue and Profit at each Hospital (Part 1) |

|

| Fig. 4: Revenue and Profit at each Hospital (Part 2) |

The figures show that the net profit at Lippo Cikarang is the lowest among all the major hospitals. Its net profit margin is only 1% of revenue. This is likely due to the high rent that Siloam pays to First Reit. The operating expense is 96% of the gross profit. In contrast, the same ratio for the other hospitals ranges from 38% to 81%, with a weighted average of 50%. A hospital that has similar revenue and gross profit as Lippo Cikarang is Purwakarta. The operating expense is 55% of gross profit and net profit margin is 10%. The information does suggest that the existing Base Rent might be unsustainable for LPKR, MPU and Siloam, and some lease restructuring might be necessary.

By right, the hospitals are very secure assets to ensure Siloam fulfils its rent obligations. Termination of the leases would lead to Siloam not being able to continue its business, which is a very serious implication. However, this does not apply to LPKR and MPU, as they have other businesses besides Siloam's business. Also, using Lippo Cikarang as an example, Siloam is not making much profit from the hospital. If First Reit insists on LPKR and MPU fulfilling their rent obligations, there is some probability of them breaching the lease agreements, as there is not much profit to be made anyway. At some point in time, LPKR, MPU and Siloam will seek a restructuring of the leases to be more sustainable. This includes Lippo Cikarang, which, while not subject to lease restructuring currently, is due for lease renewal in Nov 2025.

Another key question of this lease restructuring is whether LPKR and/or MPU will seek another restructuring if they continue to encounter financial difficulties in future, since they have already sought one now. It is very difficult to answer this question as very few persons can tell how LPKR's and MPU's businesses will perform in future. However, using Lippo Cikarang as an example, by reducing the Base Rent to a more sustainable level, there is more money left on the table to keep LPKR, MPU and Siloam from walking away.

The proposed lease restructuring is a very painful exercise for First Reit's shareholders who have been accustomed to it paying good distributions regularly. However, based on the information gleaned from Siloam's financial reports, it suggests that the rents that First Reit collect from LPKR, MPU and Siloam might not be sustainable. Reducing them to a more sustainable level might be a more equitable outcome for all parties in the long run.

This episode shows that investing in REITs is not a buy-and-forget activity. It also shows the importance of knowing your customers well.

See related blog posts: